Weekly Market Watch Week of 3/19

WEEK: 3/19/23 - 3/25/23

Last week, the banking troubles in the US and Europe caused a stir in the markets, which was a result of rapid rate hikes not seen since the early 1980s. Bringing down inflation will be costly and may lead to economic damage and cracks in the financial system. The recent events may lead to a recession, which will affect bank lending and reinforce the recession view. Market expectations for peak rates plummeted as investors hope that central banks will rescue them by cutting rates, as they did in the past. However, this is no longer a viable solution. The central banks will keep fighting stubbornly higher inflation and use other tools to safeguard financial stability. Investors need to adopt a new investment playbook and stay nimble in this new market regime.

The recent banking stresses are different from the 2008 global financial crisis, and the troubles that emerged were well-known, with much stricter banking regulations now. The markets are now scrutinizing bank vulnerabilities through a lens of high-interest rates. Here are our three clear takeaways for investors. First, stay underweight equities and downgrade credit to neutral. Second, overweight short-term government bonds, and third, prefer emerging market assets. Central banks will not try to resuscitate growth by cutting rates due to persistent inflation. Instead, they will seek to bolster the banking system while distinguishing those efforts from the need to keep fighting inflation. The article expects the Fed to press ahead with another rate hike, and the Bank of England may pause hikes next week. Finally, the article suggests that global PMIs will help gauge how much rate hikes are denting economic activity .

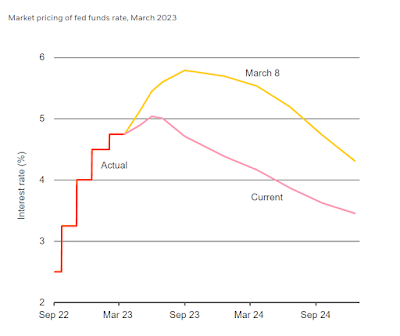

Source: BlackRock Investment Institute, with data from Refinitiv Datastream, March 2023. Notes: The chart shows the forward fed funds rate through December 2024 as implied by SOFR futures prices as of March 8 and March 17.

Comments

Post a Comment